01202 802 677

01202 802 677Help to Buy mortgage guarantee

How the scheme works

The Help to Buy mortgage scheme aims to improve the availability and cost of mortgages requiring smaller deposits. It is available across the UK and can help you buy a home with a deposit of as little as 5%.

The guarantee element is provided to your lender – not you. You apply for a mortgage from a participating lender as normal and you’ll be subject to their usual lending criteria.

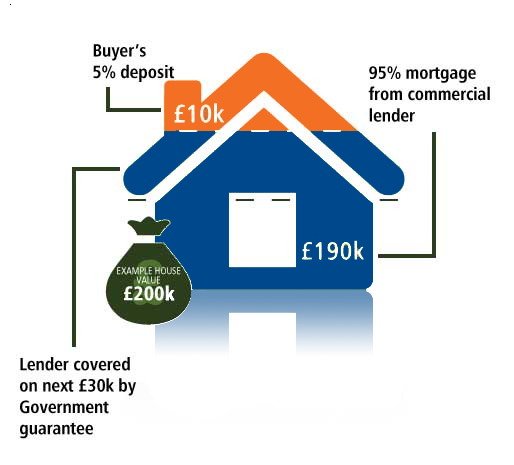

The scheme works behind the scenes by offering lenders the option to purchase a guarantee from the government on mortgages where a borrower has a deposit of between 5% and 20%. The guarantee offers lenders an ‘indemnity’ or insurance cover, which will compensate them for most of any loss they may suffer if the property has to be repossessed and there is insufficient equity in the property to fully repay the lender.

You don’t have to be a first-time buyer and pre-owned homes are eligible as well as new-build properties.

Example

If the home in the graphic above sold for £250,000, making a £50,000 ‘profit’, you’d get the entire £250,000, without having to pay back any government loan or share any profit. As you own the property fully, you receive the full benefit of any property appreciation with just your mortgage to repay as with any normal mortgage. Who is eligible for Help to Buy mortgage guarantee? Eligibility criteria for the scheme are detailed below:

- Available to both existing home owners and first-time buyers

- Buyers need a minimum of 5% deposit

- Available on previously owned and new build properties up to the value of £600,000

- Must be the only property owned by the borrower

- Available for properties in the UK

- Borrowing from a participating mortgage lender

- Buying a residential property that will be lived in and not rented out